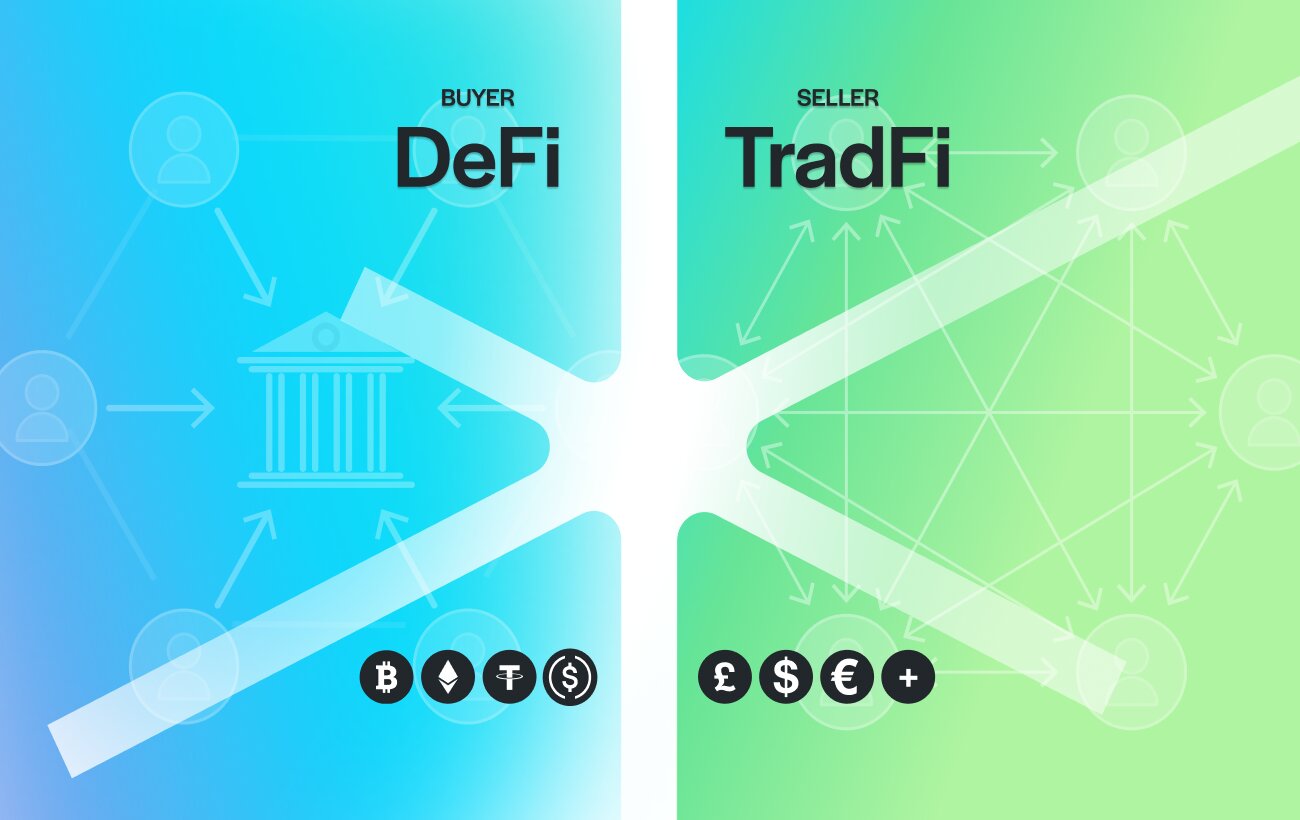

Crypto to Fiat Bank Transfers

Crypto to fiat bank transfers enable cryptocurrency to act as the funding source while fiat currency is delivered to a bank account. This payment model has become essential as crypto ownership grows faster than merchant acceptance.

Millions of individuals and businesses now hold stablecoins such as USDT, USDC, and EURC. However, rent, supplier invoices, salaries, and professional services still settle almost exclusively in fiat. Crypto to fiat bank transfers close this gap by allowing digital assets to fund real world payments without changing how recipients operate.

Why crypto to fiat bank transfers matter

Holding crypto is no longer difficult. Using it for everyday obligations remains the real challenge.

Most recipients require fiat for accounting, tax, and operational reasons. At the same time, many crypto holders operate internationally and do not want to rely on local bank accounts for every payment. Without a reliable way to settle third party obligations in fiat, crypto remains disconnected from the real economy.

Crypto to fiat bank transfers solve this by separating funding from settlement. Crypto funds the payment. Fiat reaches the recipient.

Common models for crypto to fiat payments

Not all crypto to fiat payment models work the same way. Understanding the difference is critical.

Crypto cards allow spending through card networks. While convenient for small purchases, they often fail for business invoices and cross border payments.

Merchant crypto acceptance requires recipients to manage wallets and volatility. In practice, most landlords, suppliers, and professionals do not want this exposure.

Traditional off ramps move funds into the sender’s own bank account. This works for liquidation but adds friction when paying third parties and often requires maintaining a local bank account.

Crypto to fiat bank transfers use a different approach. Digital assets fund the transaction, while fiat settles directly to the recipient’s bank account.

Why modern crypto to fiat bank transfers avoid SWIFT

Many international payments still rely on SWIFT. While widely used, SWIFT introduces cost, delay, and uncertainty.

SWIFT payments often pass through multiple correspondent banks. Each intermediary adds fees, compliance checks, and settlement delays. As a result, international transfers can take several days and incur unpredictable costs.

Modern crypto to fiat bank transfers increasingly use Global ACH instead of SWIFT. Global ACH connects local clearing systems such as SEPA, Faster Payments, and ACH across borders.

This approach delivers clear advantages:

- Lower transaction costs due to fewer intermediaries

- Same day or next day settlement in most corridors

- Higher delivery certainty once funds enter domestic rails

- Reduced payment failures and deductions

- Better transparency for reconciliation and reporting

For crypto funded payments, Global ACH provides a faster and more efficient settlement layer.

The role of stablecoins in global settlement

Stablecoins make crypto to fiat bank transfers practical at scale.

They remove price volatility and allow exact fiat amounts to be specified in advance. They also simplify cross border accounting and reconciliation. According to the Bank for International Settlements, stablecoins are increasingly used alongside traditional payment infrastructure for real settlement activity.

When paired with local clearing rails, stablecoins become an effective funding instrument for global payments.

How TrustLinq enables crypto to fiat bank transfers

TrustLinq enables crypto to fiat bank transfers through a model called crypto funded fiat settlement.

In this model, the payer funds the transaction from a self custodial crypto wallet. Fiat is then delivered directly to a third party bank account via local clearing systems. The recipient never handles crypto and does not need to change their workflow.

TrustLinq uses Global ACH rather than SWIFT wherever possible. This allows payments to settle faster, at lower cost, and with greater certainty.

Importantly, the sender does not need a traditional bank account to pay international obligations.

Crypto to fiat bank transfers versus off ramps

Crypto to fiat bank transfers are often confused with off ramps, but the difference is structural.

Off ramps move funds into the sender’s account. Crypto to fiat bank transfers settle directly to third parties. Paying a supplier or contractor is not the same as cashing out crypto.

This distinction matters for operational scale, compliance, and efficiency.

FAQs

You can fund the payment with crypto while the contractor receives fiat through local banking rails using a crypto to fiat bank transfer.

No. Many modern transfers use Global ACH and local clearing systems instead of SWIFT.

Fiat backed stablecoins such as USDC, EURC, and USDT provide the most predictable settlement.

While crypto funding is instant, fiat delivery usually occurs within one to two business days via local clearing systems.

Yes. This model supports invoices, salaries, contractors, and operational expenses without requiring recipients to accept crypto.

Turning crypto into a global payment tool

You should not be limited to a small number of crypto friendly merchants. Crypto to fiat bank transfers make the global economy accessible using digital assets.

Whether you are paying rent, settling invoices, or funding international operations, crypto can now move seamlessly into fiat settlement.

TrustLinq enables crypto funded fiat settlement to any bank account worldwide.

Spend crypto without waiting for merchant adoption.